Cautious Optimism, Improving Conditions, and What It Means for Your Next Move

The First Half Was Steady. The Second Half Could Be Better.

If the housing market felt a little quiet in the first half of 2026 — you weren't imagining it. Home sales ran close to flat year-over-year through the spring. Mortgage rates stayed stubbornly above 6%. Many buyers and sellers who had hoped for a clearer signal kept waiting.

But here's what's easy to miss in that narrative: the market held. It didn't fall apart. It didn't spike. It did exactly what a healthy, transitioning market does — it stabilized, and now it's beginning to build momentum heading into the second half of the year.

Forecasters at Realtor.com put it plainly: buyers and sellers have shown a lot of staying power. This is a market where people are adjusting and showing up rather than giving up. That's an important distinction — and it sets the stage for what comes next.

What the Forecasts Are Saying

Here's where the major economic forecasters currently land on the second half of 2026:

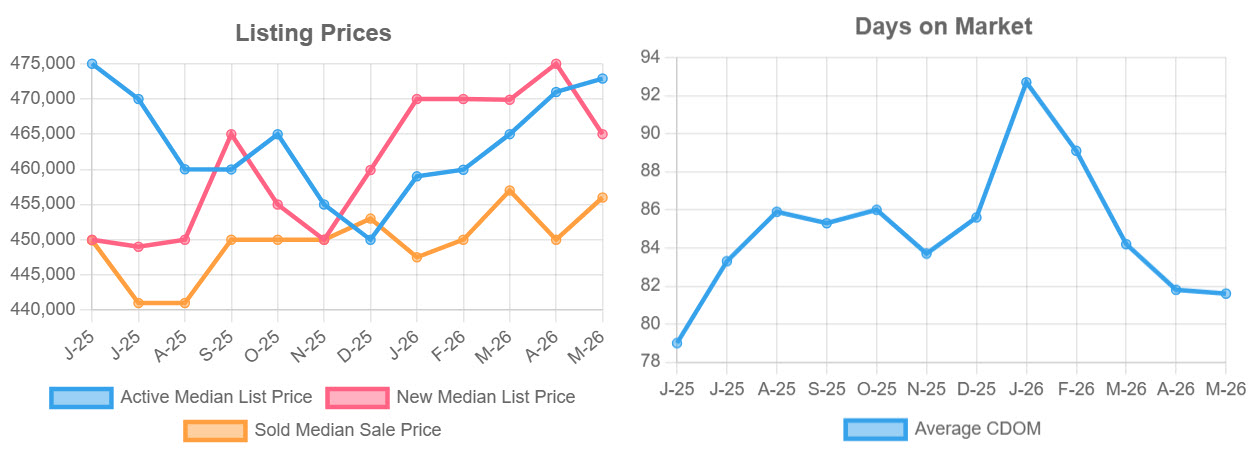

• Home prices nationally are up about 1.7% year-over-year as of mid-2026, with the average expert forecast calling for a full-year gain of around 2.3%. That means price growth would need to pick up modestly in the second half — modest, not dramatic.

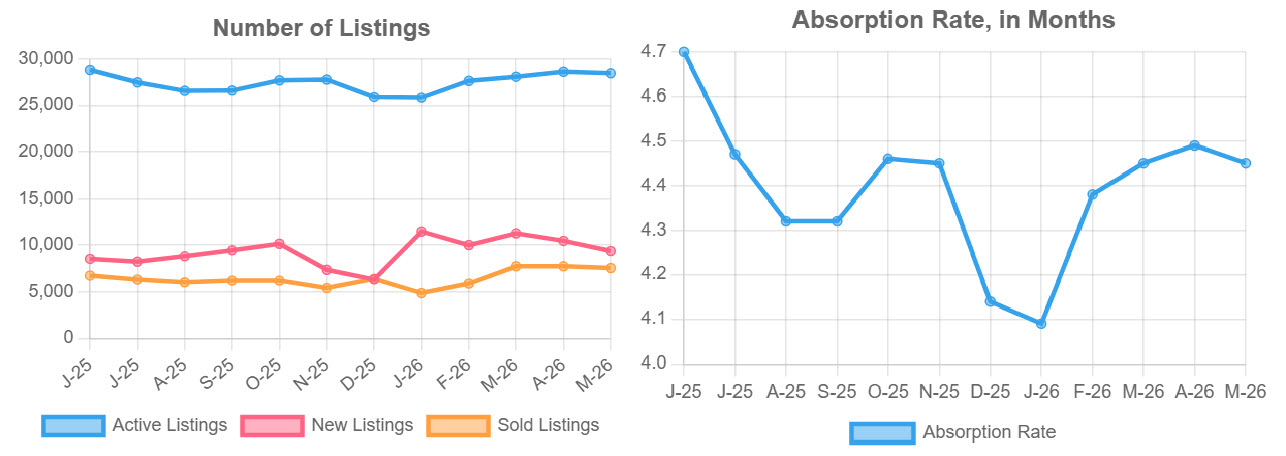

• Existing home sales are expected to improve, with Realtor.com projecting about 4.1 million sales for the full year — up 1% from 2025. Goldman Sachs projects annualized sales of 4.2 million in the second half, a 3% improvement from the first six months.

• Mortgage rates are expected to ease gradually. The 30-year fixed rate is forecast to close 2026 around 6.3%, with some projections suggesting it could dip toward 5.7% if inflation continues to cool. Even a modest decline makes a meaningful difference in monthly payments.

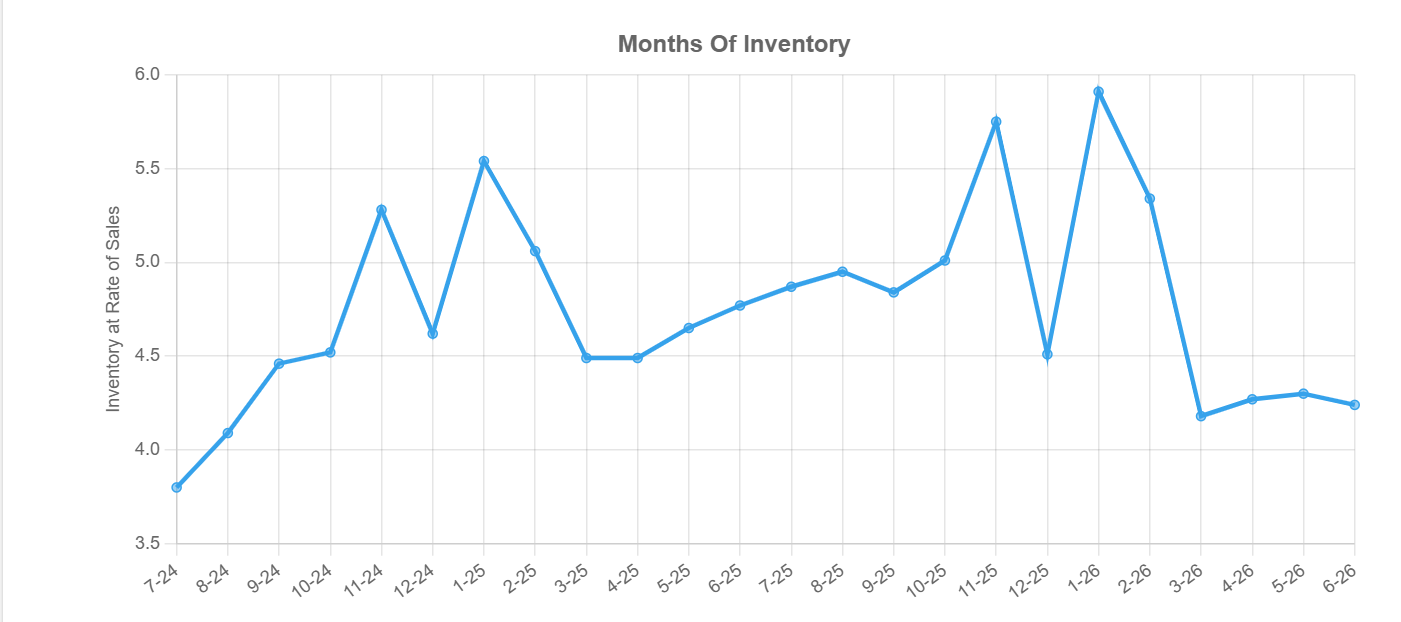

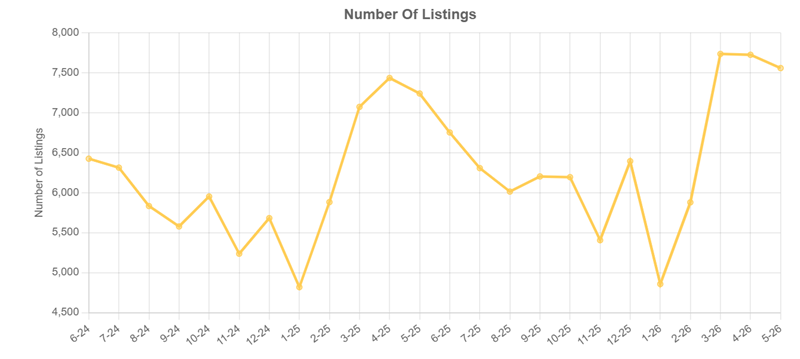

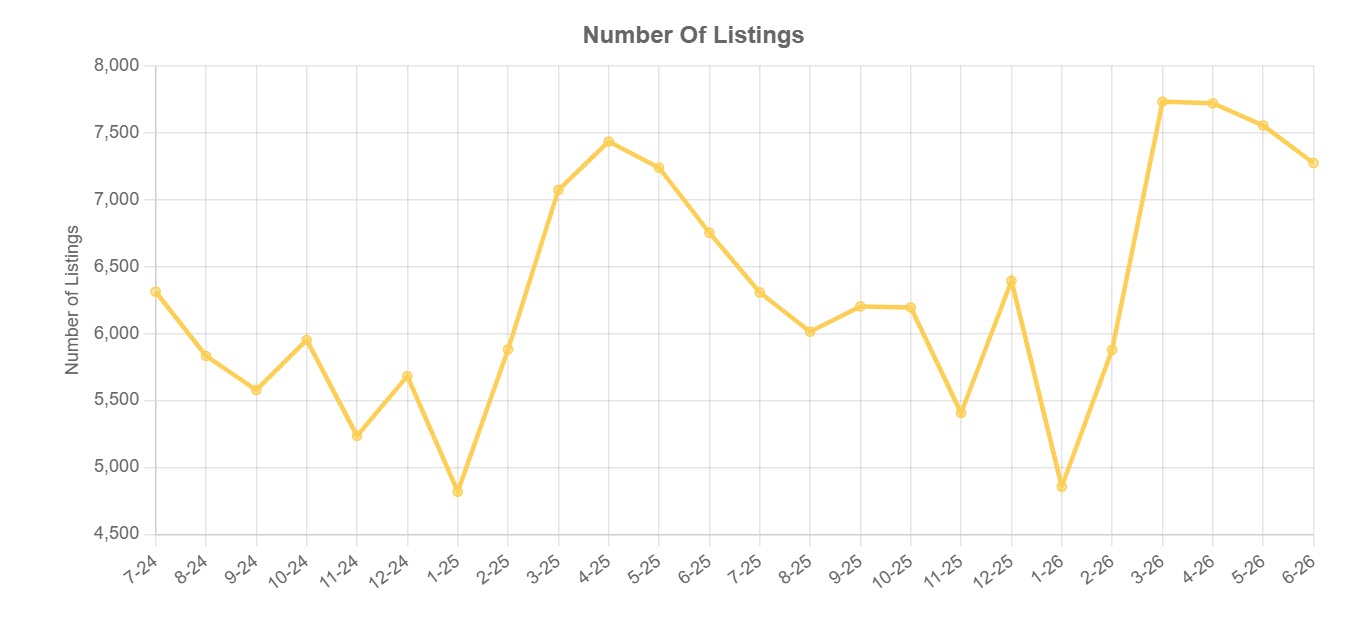

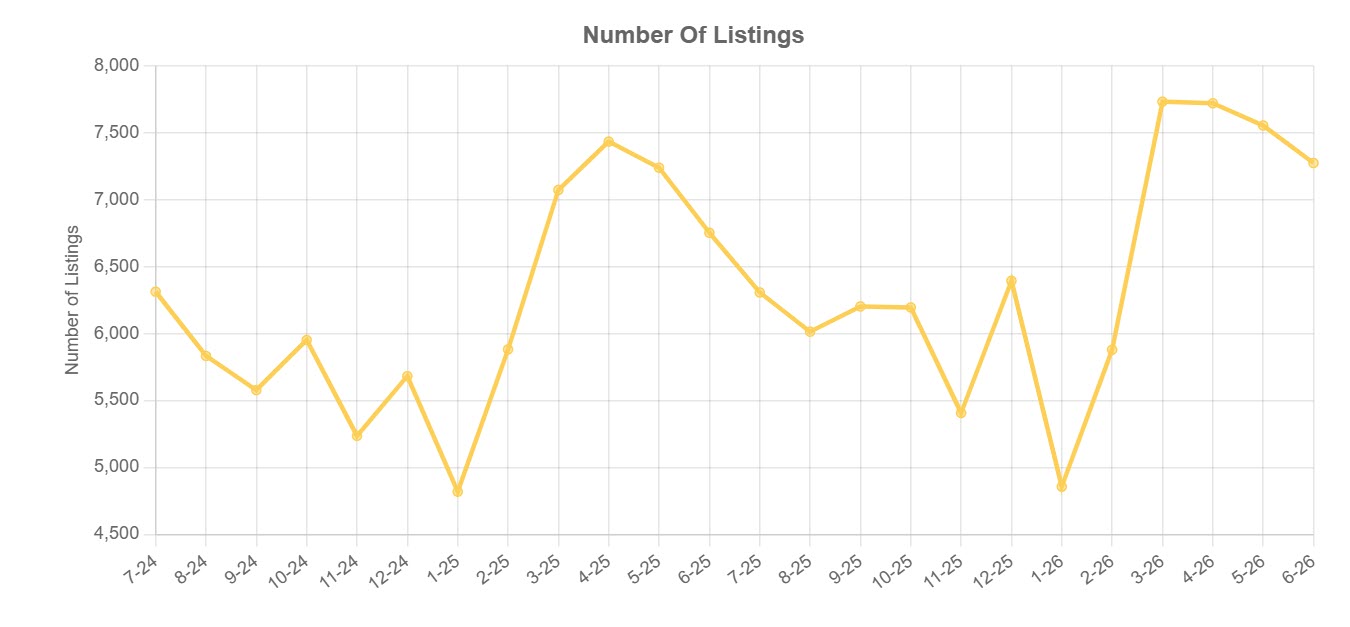

• Inventory is growing — but more slowly than initially expected. Realtor.com revised its inventory forecast to approximately 3.6% growth by year-end, down from an earlier projection of 8.9%. Fewer new listings hitting the market could provide some support to prices.

What Could Shift Things

The second half of 2026 isn't guaranteed to be better than the first — but several conditions would make it meaningfully more active:

• If mortgage rates dip even slightly, pent-up buyer demand is expected to re-enter the market quickly. Many potential buyers have been waiting on the sidelines not because they don't want to buy, but because they're watching rates.

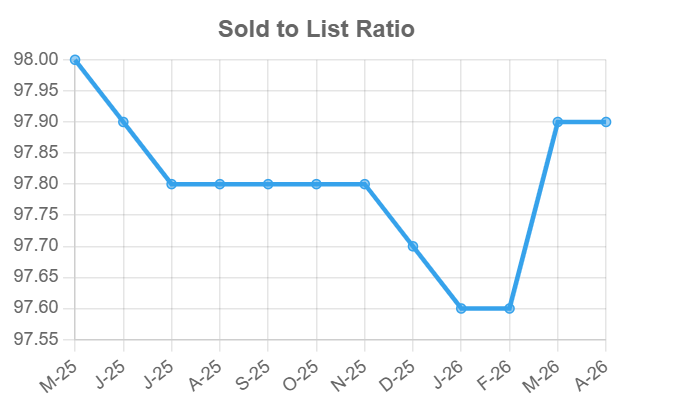

• As sellers recalibrate expectations and price more realistically, more deals are getting done. The bid-ask gap that stalled transactions in 2023 and 2024 has narrowed considerably.

• Seasonal patterns typically favor the fall market for serious buyers and sellers — less competition than spring, but plenty of motivated parties on both sides.

For Buyers: Why Waiting May Not Pay Off

It's tempting to wait for rates to fall further or prices to drop before buying. But the math on waiting is more complicated than it looks. If rates ease and more buyers enter the market simultaneously — which most forecasters expect — competition increases and so does upward pressure on prices.

Buying before that shift happens and refinancing when rates fall is a strategy that makes sense for many buyers, particularly those who have found the right home at a fair price. You can always refinance. You can't always find that house again.

The buyers who will look back on 2026 as a great time to buy are likely the ones who acted while others were still waiting for certainty that never fully arrives.

For Sellers: Price It Right and Be Ready to Negotiate

The second half of 2026 is not a market where overpricing gets corrected by enthusiasm. Homes that are listed accurately and presented well are moving. Homes that aren't are sitting — and the longer they sit, the harder they are to sell at any price.

The good news for sellers is that buyer demand hasn't disappeared. Pent-up demand from buyers who have been waiting is real and significant. As conditions gradually improve, that demand is expected to emerge — and sellers who are positioned correctly when that happens will be in a strong spot.

The key is going in with realistic expectations, a strong presentation, and a willingness to meet motivated buyers where they are.

What This Means in Phoenix, Arizona

The Phoenix metro has been tracking closely with national trends in 2026 — stable prices, improved inventory compared to the frenzy years, and buyers with more negotiating room than they've had since before the pandemic. As the second half unfolds, the Valley's strong population growth and diverse employment base remain underlying supports for demand.

Sellers in Phoenix who price accurately and prepare their homes well are still closing deals. Buyers who have been hesitant should consider that the window of relative balance may not last indefinitely — particularly if rates ease and demand surges.